The exposure of Lebanese banks to public debt and treasury bonds is equivalent to 69% of their total assets while up to US$11.8bn in Eurobonds is estimated to be held by international market participants.

by Michel Fayad

Source: Annahar

Date added: 14 December 2019

The peg between the weak local Lebanese Pound and the globally strong US Dollar is an anomaly since the US is neither the main supplier nor the main client of Lebanon. In recent months, the Lebanese Pound has weakened against the US Dollar on the black market, while the official exchange rate remains unchanged amid an increasing shortage of dollars, thus creating arbitrage opportunities.

To address the situation, the Lebanese Pound should be pegged against a basket of currencies including the US Dollar and Euro because the European Union is the main supplier and the main client of Lebanon. At a later stage, a floating exchange rate should be adopted.

The fixed rate adopted by the Central Bank of Lebanon was maintained by offering high-interest rates—paid by accumulating more debt that has been repaid by a poorer population to Lebanese banks and by banks to their depositors and to international markets.

This largest government-sponsored Ponzi scheme in history worked until the war in Syria broke out in 2011, leading to an economic slowdown in Lebanon. Since then, the Lebanese economy hasn’t expanded amid a widening twin trade and budget deficits.

Unlike Bernie Madoff's Ponzi scheme, which used a “split-strike option strategy” based on lies that affected a few hundred rich investors, Lebanon’s version of the scheme is having an impact on all of its population.

Nasser Saidi, a former BDL vice-governor (from 1993 to 2003) and former industry, economy and trade minister (1998-2000), described BDL’s financial engineering as a “Ponzi scheme” that relies on fresh borrowing to pay back the existing debt.

Nassim Nicholas Taleb, the author of The Black Swan, shared that view. In response, the legal department of the Central Bank of Lebanon said its operations were in conformity with the law as set out in the 1963 Code of Money and Credit.

Alain Bifani, the Director-General of Lebanon’s Ministry of Finance, was quoted in a Wikileaks document which dates back to 2007 as saying that Central Bank Governor Riad "Salameh has been hiding the deficit in BDL’s books by settling high-interest MOF debt and reissuing lower interest debt in the BDL’s portfolio."

Thus, a change of the BDL’s policy is required since Lebanon can no longer survive under the current rentier economic model that favors the real estate and financial services sectors at the expense of productive sectors. Lebanon must also abolish exclusive agencies and monopolies and adopt a real capitalist economy (économie libérale) that should be regulated to reduce poverty.

But first, the country's debt must be restructured.

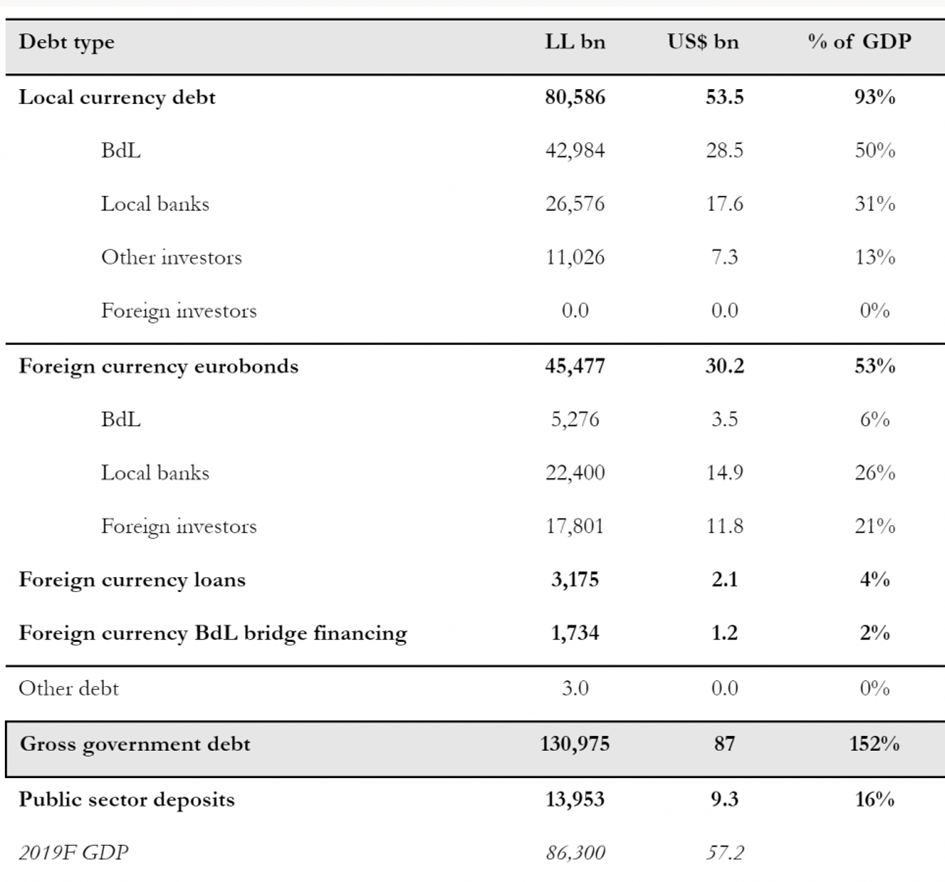

The total 2019 debt of Lebanon is estimated at US$88.4bn (154.5% of GDP), with domestic-currency debt at US$55.1bn (96.3% of GDP) and foreign-currency debt at US$33.3bn (58.1% of GDP).

The exposure of Lebanese banks to public debt and treasury bonds is equivalent to 69% of their total assets while up to US$11.8bn in Eurobonds is estimated to be held by international market participants.

According to Refinitiv data, around two-thirds of Lebanon’s foreign debt is estimated to be held by local banks, while the remainder is held by international market participants, such as Amundi, Invesco, JPMorgan, AllianceBernstein and Fidelity.

Lebanon government debt as of 2Q 2019 (Eurobond data adjusted to reflect latest figures). Source: BdL, BofA Merrill Lynch Global Research. Levels include accrued interests. All data as of June 2019, although BofA Merrill Lynch Global Research has adjusted Eurobonds data to reflect the most recent figures. % of GDP based on 2019F GDP. Other debt reflects special T-bills in foreign currency (expropriation and contractor bonds). Public sector deposits are mostly LL-denominated.

Lebanon government debt as of 2Q 2019 (Eurobond data adjusted to reflect latest figures). Source: BdL, BofA Merrill Lynch Global Research. Levels include accrued interests. All data are from June 2019, although BofA Merrill Lynch Global Research has adjusted Eurobonds data to reflect the most recent figures. % of GDP based on 2019F GDP. Other debt reflects special T-bills in foreign currency (expropriation and contractor bonds). Public sector deposits are mostly LL-denominated.

In 1967, the Lebanese Parliament passed the “Intra Law,” which set down new rules and procedures in the event of bank failures in order to prevent outright bankruptcy and liquidation. Indeed, in 1966, Intra Bank was forced to suspend payments in the wake of a run on the bank that depleted its cash reserves. Intra had only a few large depositors, limited cash reserves and long-term investments in property. This law allowed the restructuring of Intra rather than its pure liquidation: the deposit obligations were replaced with shares in a new financial institution, Intra Investment Company.

A similar law could be drafted in order to restructure the debt of Lebanon. The debt held by banks must be swapped with shares of a newly established sovereign fund that comprises:

- Middle East Airlines (MEA);

- Touch and Alfa (the two mobile operators);

- Casino du Liban;

- 20% of the future oil & gas revenues of the two blocs awarded for exploration to Total, ENI, and Novatek;

- Electricity & Water management.

75% of deposits above $1 million would be converted to equity in these banks.

The new sovereign fund and all Alpha Banks could then be listed on international stock markets including New York, London, Frankfurt, Shanghai, Hong Kong, and Singapore stock exchanges (even if they have to start by secondary markets).

-----

Michel Fayad is a civil society activist and financial analyst with experience in policy making, global strategy, and business development. He graduated from HEC Paris School of Management, the London School of Economics & Political Science and NYU Stern School of Business.